UK Economic Growth Accelerates to 0.3% in November on Manufacturing Recovery

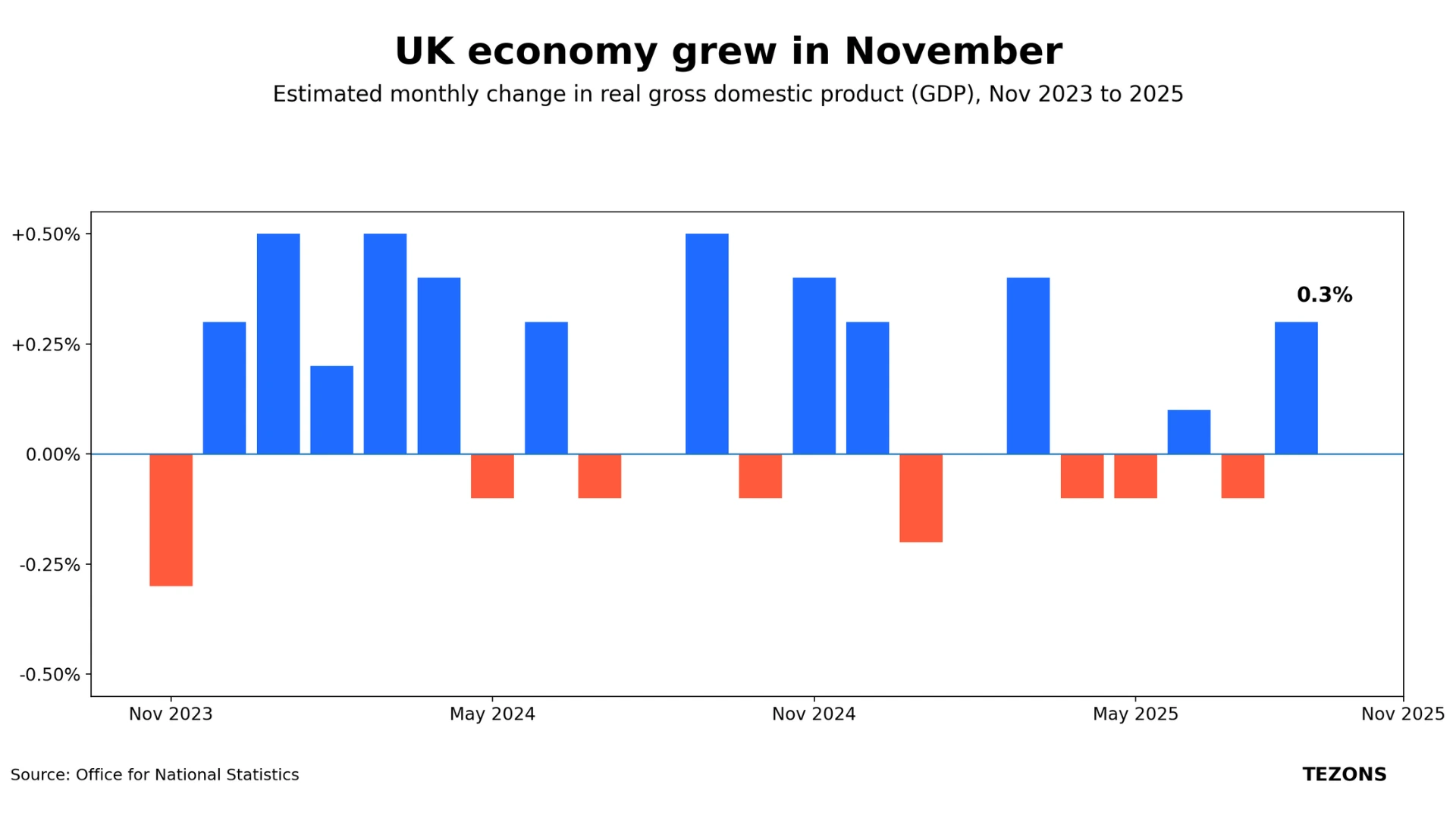

- The UK economy expanded 0.3 per cent in November, surpassing analyst forecasts of 0.1 per cent growth and reversing the 0.1 per cent contraction recorded in October

- Motor vehicle production jumped 25.5 per cent in November as Jaguar Land Rover returned to full manufacturing capacity following disruption caused by a September cyber incident

- The services sector also strengthened during November, contributing alongside manufacturing to a broader recovery in output that eased concerns about UK economic stagnation heading into 2026

Britain's economy expanded by 0.3% in November, outpacing analyst forecasts as manufacturing activity recovered and the services sector gained momentum, according to figures released by the Office for National Statistics.

The stronger-than-anticipated performance followed a 0.1% economic contraction in October and surpassed market predictions of 0.1% growth. Official statisticians attributed the improvement primarily to rising industrial output, with motor vehicle production jumping 25.5% during the month.

The automotive sector's recovery reflected Jaguar Land Rover's return to full manufacturing capacity following disruption caused by a September cyber incident that forced complete production shutdowns across its British facilities. The company implemented a phased restart beginning in October, with operations normalising through November.

Services activity also contributed to the monthly expansion, particularly within professional sectors including accounting and tax advisory. The ONS noted heightened demand for these services in the approach to the government's Budget statement on 26 November, as businesses sought guidance on potential policy changes.

The statistics office simultaneously revised its September growth estimate upward to 0.1%, reversing an earlier assessment that had shown a 0.1% decline. Over the three-month period ending in November, the economy recorded 0.1% growth compared with the preceding quarter.

Suren Thiru, economics director at the Institute of Chartered Accountants in England and Wales, described November's data as unexpectedly positive, suggesting most sectors had moved past pre-Budget concerns. He indicated the uptick made modest fourth-quarter growth across 2025 likely, noting that reduced uncertainty following the Budget presentation probably supported December activity despite illness-related disruptions affecting sectors such as education.

A Treasury representative stated the government aims to make the economy serve working households by addressing years of infrastructure underinvestment and implementing planning reforms. The spokesperson acknowledged ongoing efforts to reduce costs and inflation whilst recognising continued challenges around living expenses.

Opposition shadow chancellor Mel Stride characterised the figures as evidence of stagnant economic performance, arguing that tax increases and insufficient control over welfare spending were hampering business confidence and broader economic activity.

Yael Selfin, chief economist at KPMG UK, noted economic momentum had strengthened despite Budget-related uncertainty, with the ONS reporting in November that businesses were postponing decisions pending fiscal announcements. She identified tentative indicators of increased household spending despite relatively subdued consumer confidence.

Selfin projected continued growth momentum in coming months now that businesses face less uncertainty, with KPMG forecasting expansion across the final quarter of 2025 and positive growth in early 2026 driven primarily by business investment and public spending.

The construction sector presented a contrasting picture, with output declining 1.3% in November. The ONS recorded the industry's sharpest three-month fall in nearly three years during this period.

Ruth Gregory, deputy chief economist at Capital Economics, attributed construction weakness to unusually wet weather conditions and anticipated a December rebound. However, she cautioned that services growth merely reversed recent declines rather than signalling fundamental strengthening, suggesting November's performance represented recovery rather than sustained acceleration.

Monthly gross domestic product figures typically exhibit greater volatility than rolling quarterly data, which economists consider more reliable for assessing underlying growth trends.

Sanjay Raja, Deutsche Bank's chief UK economist, suggested the economic data should influence Bank of England deliberations regarding a potential February interest rate reduction, noting that firmer-than-expected economic conditions may reduce pressure for accelerated rate cuts.

Industry impact and market implications

The November growth figures carry significance for corporate planning and monetary policy decisions as businesses navigate the post-Budget environment. The manufacturing sector's recovery demonstrates resilience following operational disruptions, whilst the services expansion reflects demand for professional advisory capacity during periods of fiscal uncertainty. Construction sector weakness may affect housing supply and infrastructure project timelines, with weather-related impacts creating short-term volatility. The data's implications for interest rate policy could influence borrowing costs for businesses and consumers, affecting investment decisions and spending patterns across sectors. Professional services firms may continue experiencing elevated demand as companies assess tax and regulatory changes, whilst manufacturing confidence depends partly on sustained production stability and supply chain security.

LATEST NEWS

Satellites and AI used to track UK hedgehogs in bid to slow decline

Elon Musk keeps losing in court. He shows no sign of stopping

Paramount hires first consumer AI chief as Ellison bets on tech

MORE FROM NEWS

.webp)

RELATED

Subscribe for updates

Get the insights, tools, and strategies modern businesses actually use to grow. From breaking news to curated tools and practical marketing tactics, everything you need to move faster and smarter without the guesswork.

Success! Check your Inbox!

Tezons Newsletter

Get curated tools, key business news, and practical insights to help you grow smarter and move faster with confidence.

Latest News

Have a question?

Still have questions?

Didn’t find what you were looking for? We’re just a message away.